Looking inside the Russian dolls of the retirement industry – one small annuity doll and one larger “target date fund” doll - , Part 1- the US annuity market – annuity rates should be double?!?

We are all familiar with Russian dolls – dolls of progressive sizes fit into the largest doll.

The largest doll can be likened to the US retirement industry that is worth around 27 trillion dollars.

Here’s What the $27 Trillion US Retirement Industry Looks Like | ThinkAdvisor

This device has its equivalents in the retirement and investment industry. One vehicle fits in another, sometimes visible, sometimes not so much.

I have had a bee I my bonnet about the annuity market for may years. If you thought I was verbose now, check out this submission to the UK Parliament 11 years ago!

This article shows some simplified arithmetic around the annuity market. It is fungible across borders – the same principles apply. The article progresses to some notes around Target Date Funds.

Here are some country examples of annuity rates:

A few caveats to begin.

This does NOT constitute investment advice, I do not know your personal circumstances or desires or risk tolerance.

As a rule, your assets should match your liabilities – all of them.

I am not expert in annuity markets in every country, so I may have misrepresented the products referred to.

Consult your registered and authorized financial/investment adviser!

You have been warned!

From here for the US:

Best Fixed Annuity Rates Of December 2023 – Forbes Advisor

US annuity rates are a little over 5%

United Kingdom annuity rates from here – using the left hand column:

· how much a healthy 65-year-old could get for a single-life annuity with £100,000a

Annuity rates: compare the best annuity rates in 2023 - Which?

UK annuity rates are around 1% higher than those in the US. Does this reflect differences in life expectancy for a healthy 65 year old?

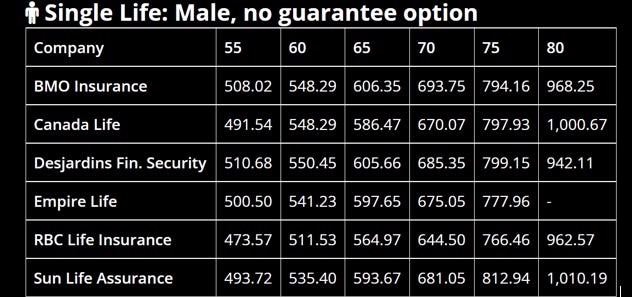

And for Canada, from here:

2023 Annuity Rates - LifeAnnuities.com

Centre column for a 65 year old, around 6% - also 1% higher than the US.

These rates are determined by actuaries at Life Insurance companies and depend on “prevailing market conditions”, government policy (Australians pay no tax on their annuities after age 70 if accumulated I the national superannuation scheme) and life expectancy.

How big is the US annuity market?

From here:

US Annuity Market to Reach $298.70 Billion by 2026 (globenewswire.com)

“The US annuity market in 2021 was valued at US$231.63 billion. The market is expected to reach US$298.70 billion by 2026. The term annuity refers to an insurance contract issued and distributed by financial institutions with the intention of paying out invested funds in a fixed income stream in the future. Investors invest in or purchase annuities with monthly premiums or lump-sum payments.”

Not massive by US standards, but around a quarter of a trillion bucks.

What is the life expectancy of someone aged 65 in the US?

From here:

Life expectancy for men at the age of 65 years U.S. 2021 | Statista

“The life expectancy for men aged 65 years in the U.S. has gradually increased since the 1960s. Now men in the United States aged 65 can expect to live 17 more years on average. Women aged 65 years can expect to live around 19.7 more years on average.”

Maybe that 17 years for men and 20 years for women has reduced slightly following the impact of C19 mRNA injections and will continue to do so – but maybe it will rebound a little as well. Making an assumption for 20 years of life to be funded from an annuity should be conservative.

Right. So that is the context, what’s the beef?

Right off the bat, consider this. If you live for 20 years ad simply took one twentieth of the money you are going to use to buy your annuity, you would “draw down” one twentieth or 5% every year and would exhaust your funds in 20 years.

A 100,000 “amount for annuity” pot would drop to zero I 20 years if 5,000 was taken from it each year.

Spa, when you see an “annuity rate” of 5%, you are simply hiring the annuity company to hold your own money and giver it back to you over a 20 year period.

What does this mean? It means the annuity company has use of all the funds you have not used for 20 years!

Over the last 50 years, the stock market has returned around 10% per annum.

What Is the Average Stock Market Return? | The Motley Fool

The long run US ten year bond yield is around 4.5% - close to spot yields.

20 Year Treasury Rate (ycharts.com)

You could reasonably expect a 60% equity:40% bond portfolio to provide returns of around 7.5% per annum.

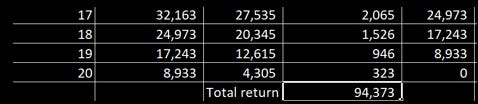

What’s the potential profit “earned” by annuity providers? You can check it out by using data tools like “goal seek” in MS Excel.

Here’s a table with that 7.5% plugged in that works out how large the annual annuity would be over 20 years of remaining life.

I will skip the intervening years:

So, instead of the buyer of the 100,000 receiving the 5-6% annuity rate and 5-6,000 bucks a year, the buyer could receive 8,256 bucks a year assuming a 7.5% investment return on the rump of the annuity pot the buyer has not “drawn down”. Instead the annuity company makes the total return of more than 96 thousand bucks for every 100,000 annuities it sells at 5%!!!

There are 2.5 million lots of 100,000 in a 250 billion annuity market – almost the entire value of a annuity is profit taken from the buyer of an annuity!

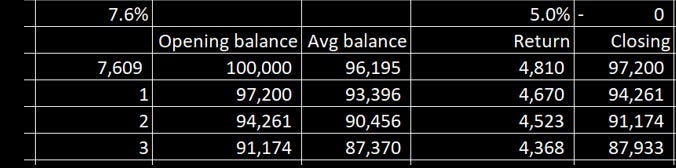

Let’s check out the sensitivity of the example and assume that the annuity rate is increased from 5% to 6% and the investment return is lowered from 7.5% to 5%.

Skip

The buyer of the annuity now gets 120,000 over 20 years from the 6,000 per annum, he investment return is lower – the annuity provider “only gets” a profit of around 60,000 bucks instead of 84,0000 bucks – disaster? Not exactly! The buyer of the 100,000 annuity gets 20,000 bucks more and the annuity provider gets around 34,000 less. Better news for the UK and Canada, but still…

Now, getting the 5-6,000 dollars per 100,000 dollars is not going to cut the mustard. Especially now that medical bills are likely to go up and the need for them is likely to increase as well, as we enter the real Public Health Emergency of International Concern – vaccine damage.

Health insurance is a “buy” right now – but it will have the same “price gouging” characteristics of the annuity market. Actuaries will estimate costs, factoring in usage rates and escalating costs of drugs and treatments.

Note that all the above does not reflect inflation or the differential and higher inflation paid by retirees.

To get protection from inflation, the annuity rate will be at least around 2% lower – so not 5-6%, but around 3-4%

What would a 65 year old need to live on in retirement? Probably around a minimum of 50,000 bucks a year.

If 100,000 buys 5,000 a year, it would cost a million bucks to get a 50,000 annual pension, but around half that if you can get a return of 7.5-8% per annum!

Some companies still offer “defined benefit” pension schemes that promise to pay annuities – even inflation linked annuities – to their employees. Most are now “defined contribution” plans that collect contributions from employees and let the take the investment risk of their choices.

That’s Part 1, in Part 2 I will take a look at Target Date Funds.

Onwards!

Please subscribe or donate via Ko-fi – any amount from 3 bucks upwards. Don’t worry and God Bless, if you can’t or don’t want to. Ko-fi donations here: https://ko-fi.com/peterhalligan - an annual subscription of 100 bucks is one third less than a $3 Ko-fi donation a week!

Nesting dolls 🪆.

Pretty sure that the Russian doll that you have used is from a company that is no longer in business.

Just sayin'