Swiss Re (an insurer of the insurance companies) – warns that life and health insurance premiums may have to increase in order to maintain solvency of life and health insurers - ignores the vaxx

“This report “The Future of Excess Death after COVID-19” from insurers Swiss Re makes clear that COVID-19 was not the main cause of excess deaths after the COVID-19 era.”

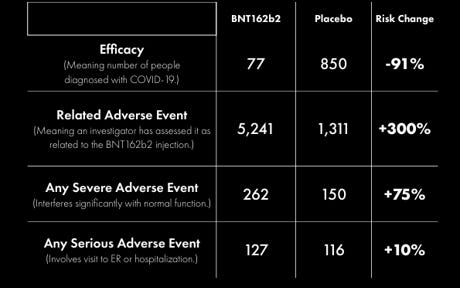

Before giving some thoughts, here is some context from an analysis of the Pfizer Phase 3 clinical trial where you can see the scale of the increased adverse events ad deaths during the two-month trial, which was supposed to be a six-month trial.

Page 12 shows the extra deaths amongst those injected and we know that the C19 cases shown is arbitrary as the injections were not intended to prevent infection, only symptoms of C19 disease. We also know that the process to make the doses was changed to the “steenking”, filthy, adulterated and contaminated “Process 2” that was actually shipped out.

These numbers should have clearly demonstrated to life and health insurance companies what was coming down the pipe that would directly impact their profitability and the need to raise premia.

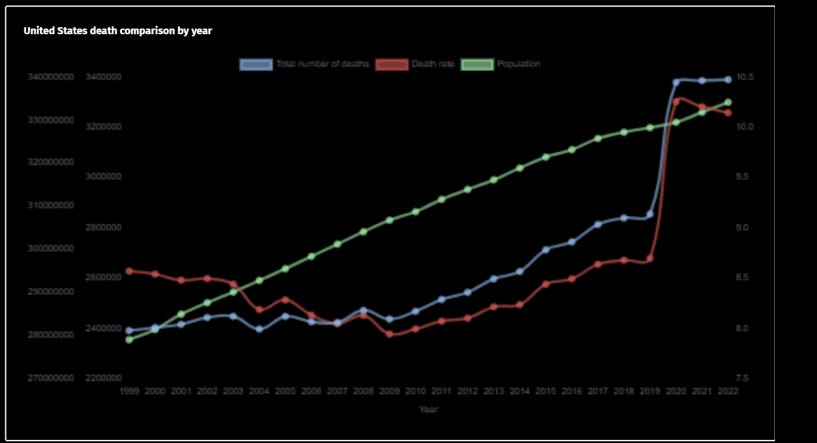

Just focussing on mortality, we can “triangulate” 700,000 dead Americas from the injections by applying.

1. a URF of 40 to VAERS of over 18,000

2. a ratio of 1 death per thousand doses with around 670 million doses administered.

We can place these estimates of the number killed by the “steenking vaccines” in the US with this chart of extra (not excess) deaths in the US pre- and post-scamdemic:

Dath rate up from 8,7 in 2019 (per thousand) to above 10 for 2020, 2021, 2022 and 2023 – an increase of around 16%. These are not “excess deaths” – they are increases in the rate of death per head of population.

Recall also that these deaths were preventable. Dr Zelenko (RIP) came up with his HCQ + AzM + Zinc protocol in March 2020 and Ivermectin was “discovered” as part of a treatment protocol – including vitamin D – by May 2020 – BEFORE the start of the clinical trials. They were a prophylactic, treatment AND cure that SHOUD have debarred the development of the EXPRIMENTAL modified mRNA injections. Note also that the CDC/FDA knew the clinical trials were showing more harm than good BEFORE they granted emergency use authorisation in early December 2020.

Okay, onto the Swiss Re report.

The report focuses on the US and the UK. It has snippets like this:

“In this research Swiss Re Institute projects excess mortality in the US and UK over the next 10 years under different scenarios, by analysing excess mortality trends globally and disaggregating the underlying factors driving them. We find that excess mortality persists today and may potentially continue for the next decade. Our general population forecasts suggest that excess mortality will gradually tail off by 2033, to 0–3% in the US and 0–2.5% in the UK. In comparison, by our calculation excess mortality in 2023 was in the range of 3–7% for the US, and 5–8% in the UK.”

For the US, this would represent a sharp decline I the rate of EXTRA deaths from around 15%. Not that these numbers impact only life insurance profitability from premia levied. Some life insurers have already raised rates to reflect the extra death rate.

Perversely, check this out from Brave browser answer to “how much have US life insurance premiums increased since 2019”:

“In summary, while the life insurance industry has experienced fluctuations, the aggregate life insurance premiums written in the US decreased by 19.1% from 2019 to 2023. This decline is primarily driven by a 25.5% drop from 2022 to 2023.”

Weird, right? Unless the extra few million or so extra deaths were paying for a lot of life insurance!

The report has a set of charts, modelling data in various countries across different scenarios:

By clicking on the tab with the scenario “Early peak – slow run-off” we get this chart:

Countries used (fitting?) the scenario are France, the UK and the Netherlands. Here’s a few data points:

The US is under the “Early peak – quick run-off” tab, along with Italy and Belgium:

Here’s some data points:

US extra deaths from the “deadorkicking” chart above are at around 15% extra deaths for 2023! IS this the same sort of “fake achievement” claimed by the Democratic Party around inflation dropping to 3% whilst locking in30% higher prices over the previous 3 years? Inflation should be NEGATIVE to return prices to around pre-scamdemic levels. So should federal spending have returned to around pre-pandmeic levels, instead of going up even further. Inflation hasn’t turned negative, either has federal spending – is this the same effect as the reduction in the rate of “excess deaths” too 5%, despite extra deaths being maintained at 15-16% above 2019 levels?

Never mind, these Swiss Re guys are going to be “best in breed” and have real money on the line, so maybe they know something we don’t!

Here’s their narrative:

“We developed a standardised methodology for cross-country comparison of pandemic-era excess mortality. This shows four key patterns: in the US, excess mortality peaked early and declined rapidly. In contrast, the UK’s early peak was followed by a slower decline.

Australia delayed its peak by close to two years and achieved a quick decline.

Canada reported very low excess mortality in 2020, with a gradual increase peaking in 2022 and 2023, reflecting a late peak and slow decline.

These patterns correlate with countries’ responses to COVID-19, specifically the timing and effectiveness of preventive measures and the rate at which mortality returned to expected levels.”

We will have to wait for the next report from Denis Rancourt next month for some more insights!

Here’s the real meat!

“The pandemic has significantly altered the causes of excess deaths. We analysed the evolution of major causes of death from 2020 in developed countries that report such data.

Respiratory mortality accounts for the largest share of excess deaths each year since 2020, as expected. However, we find evidence of inconsistency in the causes of death recorded over this period, with signs that other causes of death were misclassified as COVID-19.

The UK and US data shows a large, unexplained jump in deaths attributed to cardiovascular disease (CVD) since 2020.

Some countries also reported excess mortality over a pre-pandemic baseline for other major causes of death, such as cancer.”

This corresponds exactly with the work done by John Beaudoin (of “The Real CDC” fame), who, after analysing millions of death records across several states found that there was a huge switch from respiratory deaths in 2020 to circulatory causes from 2021 onwards!

This coincides with the roll-out of the “steenking” experimental “vaccines”. No doubt the CDC/FDA will claim this is a feature of a new variant.

The statement “other causes of death were misclassified as COVID-19” corresponds to my belief that a significant proportion of deaths were attributed to C19, instead of “usual causes” in 2020, and then in another huge de facto “medical fraud” – deaths from the C19 injections were falsely attributed to natural causes from 2021 onwards.

The report concludes with this:

“Based on current medical trends and expected advancements, we conclude that COVID-19 is still driving excess mortality both directly and indirectly.

In the long term, lifestyle factors that contribute to poor metabolic health and lead to obesity and diabetes may become another compounding factor in population excess mortality.

Insurers may wish to continue to monitor excess mortality and its underlying drivers in the general population closely, as well as the differences between general and insured populations.”

This to me causes the report to fail. It avoids the giant syringe in the room – the filthy, “steenking”, adulterated, contaminated, experimental modified mRNA injections.

It also has a glaring omission that you would expect “Life and Health” R&D managers and analysts to cover. They covered excess mortality, but not the rising costs to health insurers of the deteriorating health of those paying health insurance premia.

The Pfizer Phase 3 clinical trial indicated that around 5,200 out of around 22,000 double dosed injection recipients suffered adverse events. Say that each adverse event was unique to a single individual = 5,200/22,000 double dosed victims = 24% of those injected.

Around 270 million Americas received at least dose – implying that around 60 million suffered some sort of adverse evet that may have manifested or be about to manifest. Some fraction of this umber will have claimed health care from their insurance company or be about to.

No mention of this in the report.

– remember these were amongst a healthy, uninfected population between the ages of 15 and 60 – no pregnant women, no-one with the 2-6 co-morbidities aged 65 or above – the most likely to die from C19 or be killed by treatment protocols.

Onwards!!!

Please take a paid subscription or forward this article to those you think might be interested. You can also donate via Ko-fi – any amount from three dollars upwards. Ko-fi donations here: https://ko-fi.com/peterhalligan

My employers health insurer last year ran, out of the blue, a survey re staff health but buried in the survey were a number of very focused questions re the covid jab.

I refused to complete such but I was convinced the real reason for the survey was reg insurer knew there was a problem and was seeking to assess future risk/ premiums

Ed Dowd has been very clear about the actuarial data and it’s far from good.

My employers health insurer last year ran, out of the blue, a survey re staff health but buried in the survey were a number of very focused questions re the covid jab.

I refused to complete such but I was convinced the real reason for the survey was reg insurer knew there was a problem and was seeking to assess future risk/ premiums

Ed Dowd has been very clear about the actuarial data and it’s far from good.

If they can't get us one way, there's always another! 😈