Proxy voting – who votes at annual and extraordinary shareholders meetings? Shareholder participation and “activism” required to rescue Pfizer and save lives

First of all, I provide a brief resume so that you can judge whether I am qualified to “vent” o such matters.

Next, I will pose a question “If you own shares in a company you can propose resolutions at company shareholders meeting and vote on the proposed resolutions of the company at these shareholders meetings – doo investment managers vote n your behalf without consulting you – BY PROXY – without consulting you?”.

I spent four decades in the investment management industry. I worked for four companies based in London, Chicago and Auckland (with a short stint at Bloomberg). I have travelled hundreds of thousands of miles and now live in an attic in central London, dealing with the aches and pains of those in their mid-60’s I have never been tested for C19, or received any C19 injections. I did take the required injections required for travel to sub-Saharan Africa twenty or so years ago.

I was an investment manager of sovereign wealth, pension, insurance and trust funds, I have been a licensed stock exchange operator and broker of derivatives and securities and finished my career at an investment consultancy helping large owners of capital select cash, fixed income, liability driven investments, target date, balanced. index tracking funds and “transitions” from one manager to another. All with the objective of reducing costs and achieving the best possible absolute and relative returns within a risk budget. I occasionally helped out with research on the largest US insurance companies, research on equity, hedge ad real estate funds, especially where there was a fixed income element.

I had a hand in the passive and active management oof trillions of dollars of client fuds requiring the research and monitoring of even more trillions of bucks of tens of thousands of investment manager “products”. Quite the task, requiring quite the effort of a large team, where your quality is always o display, or not! It is very hard to argue with the facts displayed n a regular basis.

During these decades – at all times – every investment and every decision was challenged by new ideas against old, new opportunities against old – shift happens. There is no such thing as a “fire and forget” decision. As I write this for some reason this tune runs through my mind on all the different sorts of relationships comes to mind

Olivia Newton-John & John Travolta - You're The One That I Want (1080P) (youtube.com)

But nothing last forever and the pursuit of excellence requires fishing in a very large sea!

The fundamental basis for assessing investment managers and the likelihood that they will deliver what they claim is research. Hours of research gathering data, analysing it ad “pitching views” to others who check and independently confirm, rebut or qualify those views – in order to establish the initial rating – and then actively monitor views against changes and on a regular basis. These investment views are used for the selection of investment managers and the regular reporting of their performance to clients.

K, with that out of the way, one aspect of investment that received zero attention was proxy voting of client assets managed on an agency basis by investment managers.

We are all familiar with voting at shareholders Annual and Extraordinary General Meetings. Resolutions are proposed by the board or by shareholders and shareholders vote to accept or reject them.

Investment managers are agents of their clients. In theory, investment managers can influence the business strategy of a company by checking out the company (I the same way that investment consultants check out investment managers) – with on-site meetings with management, staff and inspecting facilities. Investment managers might say “That is not something I could recommend” to a business/company “so you need to change that before I give you my clients money” or it, in theory could vote for or against a resolution at a company’s annual (AGM) or extraordinary general meeting (EGM).

So, herein lies the rub. The investment manager is an agent – not the owner of the capital of the client.

In theory, an investment manager can only vote at an AGM or EGM based on the NET views of ALL clients,

The equivalent would be a petition that collected signatures FOR and AGAINST a citizen petition which required 100,000 NET votes, not just those votes FOR.

One can imagine a vote at a Pfizer EGM which said something like *for a two-dose regiment with one death per thousand doses).

“The company has around 50 million individual shareholders investing via thousands of investment products and the company has around 100,000 employees – it is likely that the administration of more than 100 million doses of its mRNA products have killed 100,000 shareholders and employees AND have caused 1.3 million life altering events plus half a million-life threatening adverse events.

PROPOSED: the company immediately cease the production of mRNA products and set up a shareholder and employee compensation fund with properly selected Trustees for a maximum of 1 million dollars for each death, 2 million dollars for each life altering event and 5 million dollars for each life-threatening events suffered. “

The compensation numbers are arbitrary – but even a tenth would be something.

Back to the Proxy Voting issue.

Shareholders own the company and in Pfizer’s case this has been their experience:

Pfizer has a market cap of 150 billion dollars - around the same amount it made frm its mrNA sales - and has not improved in share price in 25 years. You would think the owners of the company would have something to say about that – you know – “shareholder activism” and such. Where is the evidence of a successful strategy that meets the quality demanded by buyers of its “treatments”? This is even before questions that could be asked about its criminal record ad massive fines.

Over this 25-year period the Dow Jones Industrial Average (DJIA) has risen from around 10,000 to around 39,000. Even the DJIA sacked Pfizer frm its index of 30 companies back in 2020 - along with Exxon and Raytheon.

No questions from the shareholders of the company? Maybe they are masochists intent on being “woke”. In my view, Pfizer is a crap company, making crap products with crap management.

If ever “shareholder activism” was needed to turn the company around before it goes tits up, it is now. 150 billion dollars of capital could be put to far better use.

I posted this article in December 2022:

In it, I linked to this:

Which has this summary:

“SUMMARY: The Securities and Exchange Commission (“Commission”) is publishing supplementary guidance regarding the proxy voting responsibilities of investment advisers under its regulations issued under the Investment Advisers Act of 1940 (the “Advisers Act”) in light of the Commission’s amendments to the rules governing proxy solicitations under the Securities Exchange Act of 1934 (the “Exchange Act”). DATES: Effective September 3, 2020”

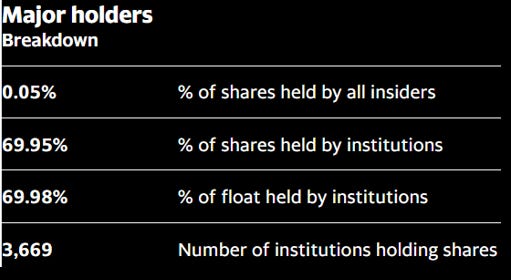

Let’s look at the largest shareholders of Pfizer:

Pfizer Inc. (PFE) stock major holders – Yahoo Finance

70% of Pfizer is held by “institutions” – which means that 30% is not.

Which institutions?

More than 26% amongst the top 4 “institutions”.

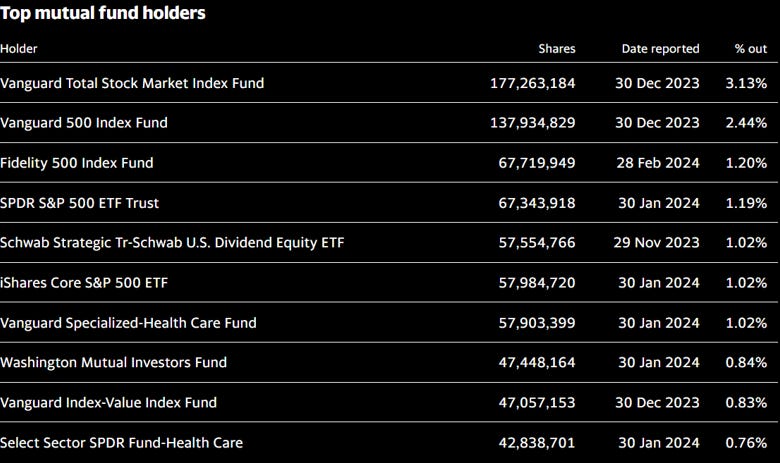

Plus, these mutual funds:

Another 8% amongst the top five. There is some overlap between “institutions” and “mutual funds”, but the important poi to keep in mind is that the holdings of say, BlackRock, in Pfizer arise from a whole host of different “investment products”. The source of those funds investing in those products might be a few hundred company pension plans, a dozen ETF’s or Target Date Funds or another dozen different index tracking funds and so on, sourced from US and Global investors.

So, who gets to vote at AGM and EGM’s – who gets to propose a resolution?

Most clients – the actual owners of the shares – could give two hoots about AGM’s and EGM’s. Occasionally the issue becomes vital ad “shift happens” – like Texas sacking BlackRock for advocating against the interests of the Texas oil and gas industry.

Check this out:

The controversy over proxy voting: The role of asset managers and proxy advisors (harvard.edu)

It has these authors:

Posted by Jan Krahnen (Goethe-University Frankfurt), Arnoud Boot (University of Amsterdam), Lemma Senbet (University of Maryland), and Chester Spatt (Carnegie Mellon's Tepper School of Business) , on Monday, January 30, 2023

From the Abstract:

“In this statement, we assess the role and power of proxy advisors and asset managers in corporate governance, an industry that is characterized by a limited number of voting advisory firms (ISS and Glass-Lewis), accompanied by the growing dominance of index investing in an industry with a few large asset managers, such as BlackRock, Vanguard, and State Street.

We discuss the business model of proxy advisory firms and contrast its objectives with those of asset managers in the context of the informational screening/filtering role and voting analysis.

This discussion concludes with a set of policy recommendations, such as: (a) requiring disclosure of advisory firms’ other businesses, (b) increasing the transparency of the business model of proxy advisory firms, particularly around the rationale for their general guidelines for voting recommendations, (c) ensuring that the regulatory burden on proxy advisory firms does not discourage entry, and (d) increasing the regulatory oversight of the voting process with a view to incorporating investor preferences in proxy voting.”

Not much on individual shareholders ability and capacity to receive information on upcoming AGM’s and EGM’s or how to propose and vote on regulations or to actually issue an instruction to an investment manager.

For information, I personally run my own pension plan via a “platform” and have gone through the procedure to vote at an AGM.

Here’s a few extracts from the last link:

“The proxy ballots are received as part of a proxy statement, which includes board recommendations for a “yes” or “no” vote. Thus, proxy voting is a mechanism that allows shareholders to influence company strategies and activities. More recently, they have become tools to challenge corporations on environmental, social, and governance issues.”

Note the term “shareholders” not “investment manager”.

“Reducing managerial effort in acquiring information is generally not an option because the SEC requires that mutual fund votes be publicly available. In addition, asset managers are expected to put into place well-designed policy and procedure guidelines for proxy voting and may face potential scrutiny from investors.”

“Proxy advisory firms specialize in conducting due diligence related to voting on agenda items at annual shareholder meetings of publicly listed firms.”

So, another set of advisors give their views on resolutions at AGM/EGM’s. This doesn’t result in an actual vote – only the shareholders or their proxies can do that.

Here are the recommendations:

“First, proxy advisory firms play a crucial role in corporate governance and the industry is characterized by low competition, effectively a duopoly. Given their central role in the proxy voting process, the accountability of these proxy advisory firms is crucial.”

A duopoly - ISS and Glass-Lewis

Here’s links to their websites.

Proxy Voting Services | ISS (issgovernance.com)

By the way, my article was triggered by the announcement that five large investment managers had withdrawn from a cartel promoting DEI/ESG BS.

If thy do “gush” over DEI/ESG ask them what impact their approach has o costs of investments and the companies invested in, the impact of performance ad risks and the basis/evidence of this.

This approach is the same that can be taken in all Federal, State, City and Local jurisdictions.

If there is no supporting evidence for cost savings and improved outcomes (the view being out forward stats that money does not matter, nor does evidence) you know you are being assaulted by a Cult that is acting in an “arbitrary and capricious” manner. Tell them to “woke off”.

There was a link to the “Get work, go broke” cartel and in that link, there was sub-link to this:

Proxy Season | Climate Action 100+

“2024 PROXY SEASON & FLAGGED SHAREHOLDER VOTES

Climate Action 100+ flags key shareholder proposals and other votes for investors to take into consideration during proxy season”.

We all know about the proxy wars in Ukraine, Syria and Gaza where foreigners fight each other and locals for “bragging rights” and to test equipment in a life fire environment – but there are also “power by proxy votes” and bear watching.

If you are an owner of/investor in a target date fund or 401k plan or an investor in index and active funds vehicles – you OWN shares in the company that the investment manager invests ON YOUR BEHALF in accordance with Trust Deeds and investment management agreements.

You ow the shares NOT the investment manager. You can vote your shares and influence the company rather than the investment manager.

You pay fees to the investment manager to manage investments on your behalf – make sure that the investment manager is not acting against your interests by following some faux climate science or facilitating illegal immigration or creating deadly injections.

Now, about the shareholders of all those other companies in the mRNA supply chain…

Onwards!

Please subscribe ten dollars a month or annually for 100 bucks. You can also donate via Ko-fi – any amount from three dollars upwards. Ko-fi donations here: https://ko-fi.com/peterhalligan

Peter in other words vote your shares.?..are these things even ON the proxy?/ I mean I've never even seen dei on my shares..just election of officers etc..share buybacks. How the he'll do we get this info? They don't mail the proxy out anymore. Can you do a guide for 7s that now have to get everything on line I. Thousands of dull pages?